I love making my Finance Storyteller YouTube video content on finance, accounting and business topics that are of interest to people. It’s amazing how some topics can far exceed expectations in terms of the number of views and comments, like this video on the financial term “Equity”! Enjoy watching!

Categories

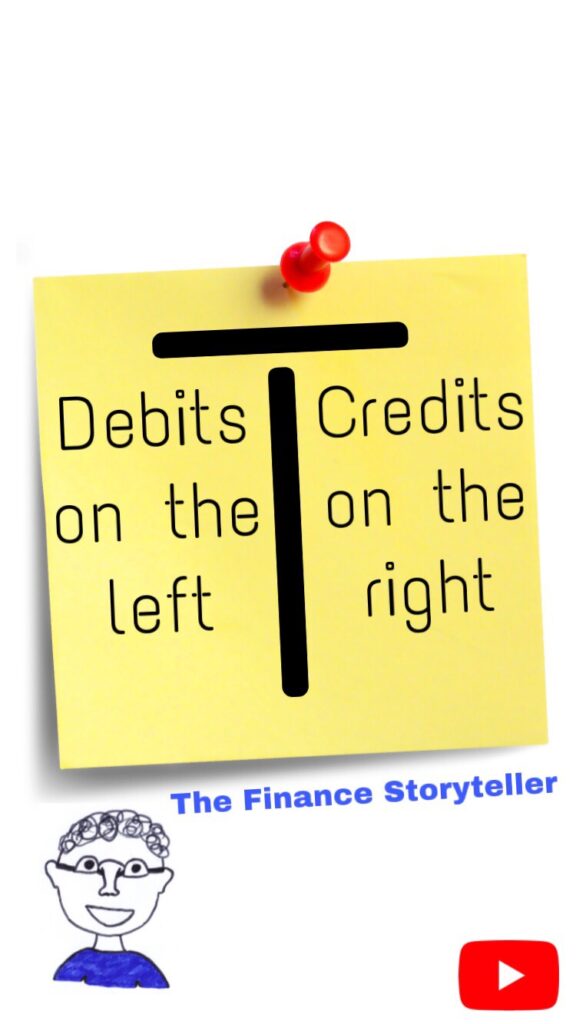

How to learn finance?

Categories

Most popular Finance Storyteller video

Categories

Financial ratios explained

Categories

New channel trailer

My new Finance Storyteller YouTube channel trailer captures very well what I am trying to achieve: helping you learn the business vocabulary to join the conversation with the CEO at your company, and enable you to make better investment decisions on the stock market! Look forward to hearing your comments.

Categories

New Finance Storyteller videos

I have been adding a lot of new videos to my Finance Storyteller YouTube channel over the past months, up to a total of 44 now on a wide variety of topics. One of these recent videos, on the very useful analytical tool called DuPont analysis, has been doing particularly well in terms of number of views, and ranking in search results. Enjoy!

I have seen a lot of companies where the CFO has trouble getting his or her C-level peers, let alone employees in general, focused on the big metrics that really matter. Here’s a video that could help communicate to both your finance team and non-finance colleagues what Free Cash Flow is, and how to impact it.