Video #11 in the Finance Storyteller series, one that affects business travel in many corporations: the Q4 travel freeze! Is it worth implementing it, to emphasize cost-consciousness? Or does it do more harm than good? Find out the pros and cons in the video below.

Category: Travel

In the “Business” and “Finance” sections of the site, I am sharing samples of my work: stories I tell during the training courses I deliver. The “Travel” section is about a key part of the “how” of being a trainer: the wonders of business travel.

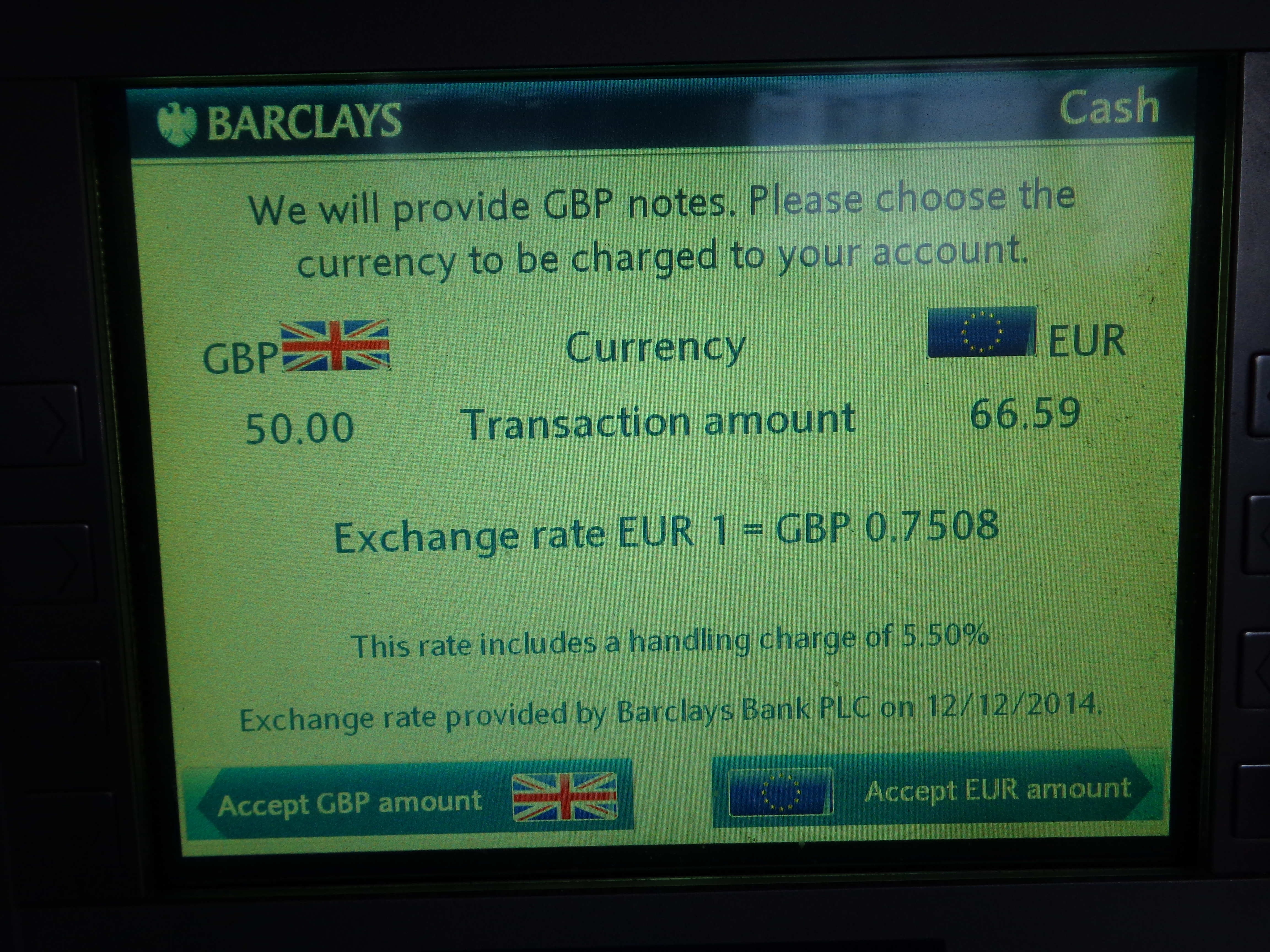

“We will provide GBP notes. Please choose the currency to be charged to your account.” This question (or a variation on the theme) is asked time and again to travelers like myself that withdraw cash from an ATM abroad. So what do you choose? The button on the left in the screenprint below, which leads you to be charged by the foreign bank in the foreign currency of the country you traveled to (and then have your home country bank convert it to your home currency), or the button on the right which will have the foreign bank convert to your home currency directly? Yes, please read that question again, as it takes a significant amount of brain energy to think through, especially if you are tired from travel and jetlag.

Well, says the average traveler, in the end the ATM withdrawal will have to be charged in my home currency to my bank account anyway, so I might as well have it done right now by this friendly foreign bank, go for the easy road of convenience and get it over with, choose the familiarity of a currency that I know rather than a currency I don’t know so well, so let me press the “Please convert” button on the right. Many foreign banks nudge you strongly towards this option by using words like “guaranteed rate” to instill a sense of safety and comfort.

The startling reality is that having the foreign bank convert the currency for you (the button on the right) is the far more expensive option! And I am trying to figure out which “service” these foreign banks are trying to convince me they should be charging me for. A basic economic premise is that the higher the value you provide, the higher the fee or price you can charge to your customer. However, if you do not provide value to me, then I do not pay you. The foreign bank (in the case of this example Barclays UK) is pretending to sell you “security, comfort, and risk management”, when all they really do is charge you a handling fee for currency conversion which you can easily avoid by having your home country bank (in this case ING NL) do the conversion for you for free at a more favorable rate. At least Barclays discloses their conversion surcharge in a reasonably sized font, so if you bothered to think it through you could figure out what this would cost you. A less respectable Hungarian bank recently made me an offer of 280 HUF to 1 EUR “pre-converted”, while I knew the actual exchange rate was a much more favorable 305 HUF to 1 EUR at my home country bank, so I happily declined. As you cannot assume that the average traveler knows these rates by heart, I am of the opinion that a bank should clearly spell out what the ATM user’s options are, and what they will cost him. Or even better, not even complicate things by offering the “pre-conversion” option, but instead plainly stating that the foreign bank charges the exact amount of foreign currency withdrawn to the home country bank who will then proceed to do the conversion at spot rates.

You could argue that withdrawing cash from an ATM is terribly old-fashioned, and you should pay electronically whenever and wherever you can. Unfortunately, the same FX scam applies to electronic transactions as well, in an even more blatant form. I visited Turkey recently, where upon checking out from the supposedly respectable Hilton hotel, I chose to pay by creditcard. The receptionist handed me the terminal in order to input my security code, and without even asking me had preselected the option without my consent to have Garanti bank convert the Turkish Lira amount to US dollars (why would I ever want that when my base currency is Euro?) at a 3% markup. I assume Garanti somehow shares this commission with Hilton, to align the incentives (against the customer). My home country bank then had to convert these US dollars to my home currency of Euro. Direct conversion from Turkish Lira to Euro by my home country bank would have saved me €16. Sure, losing €16 will not bankrupt me, but I’d rather spend it on a cup of tea and some chocolate.

It saddens me that banks try to make money off transactions where no real value is provided to the customer. I had hoped that their ethical standards and commitment to transparency would have improved after all the scandals in the past decade. Yes, it is only a relatively small amount per customer, but this scam does add up with a high transaction volume.

So, next time you’re in front of an ATM abroad, press the “Decline” option when they make you an offer to “pre-convert”.

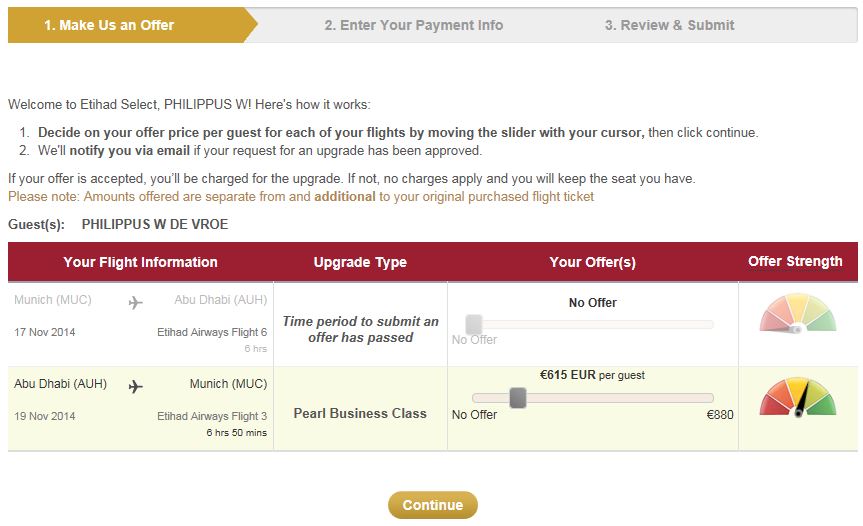

While other airlines only send lame e-mails with offers to book a car or hotel connected to your flight, Etihad has a more exciting question: would you like to bid for an upgrade to business class? If you bought an economy class ticket, Etihad will “auction” upgrades to business class for each leg of your journey. The process is in three easy steps: make an offer using a slider that indicates the offer strength, enter credit card details, review and submit. The airline will then notify you via e-mail if the upgrade request has been approved (and only then charge you).

Easy to use, and I would gladly participate if I could make a token low bid of let’s say €100 or €200 with a 10% or 20% probability that I would be lucky enough to get a seat. In other words, a “small investment, huge pay-off” bet. An offer strength indicator indicates the range of past successful offers for similar flights. Unfortunately, in my case, the slider tool does not allow a bid below €560 per leg, which would get me into the “red” category (this translates to me as: unlikely to be accepted). Starting at €595, you get into the “yellow” category (suggesting you have some chance of acceptance), and starting at €765 you are in solid dark “green” (suggesting it is highly likely that the bid will be accepted).

Frequent travelers have posted tips for successful bidding on the internet, such as:

- Look at what it would cost you to purchase the business class fare

- Bid slightly over the minimum bid

- Check how full the flight is. Make a pretend booking online, in both business and economy, so you can get to see the seat map for each cabin. If business class if empty your chances of an upgrade are good. If economy class is super full, your chances of an upgrade are quite good as airlines overbook flights all the time so freeing up your economy class seat could help.

- Decide what the upgrade is worth to you.

- The kind of ticket you purchase may matter.

- Your frequent flyer status with the airline may count.

Given that my original economy ticket was €988 roundtrip, I am not feeling I get a good “deal” here, as an economy ticket plus two upgrade bids would not be significantly cheaper than booking a business class ticket from the start.

In short: I love the concept, a nice incremental business model that could generate a good amount of additional revenue for Etihad by getting already “captive” economy passengers into those empty business class seats, but the deal has to make the customer feel he “wins” as well versus walking up to the ticket desk at the airport and buying an upgrade there.